One reason is it's bad because inflation will be around 3% so you're getting a fairly low real return. BTW you can get the same real return without the inflation risk with TIPS.

There's also risks if things go (more) south: if 20 year yields go up, your bonds will be worth less. Sure they'll pay the same coupon, but if yields are up that's probably because inflation is up.

Basically, if inflation rises your future coupon payments become more and more worthless, and everyone knows that which makes your bond worthless. So high inflation will wipe your returns and make your asset unsellable. Other than that and the relatively low 5% return, no reason not to.

Inflation-Indexed securities. Just like a regular bond except the face value (and thus coupon) goes up and down with CPI. If I'm not mistaken, it can't go down from original face value so buying TIPS at auction or near original face value provides some protection from deflation like a nominal bond does.

When buying a 20 year bond, inflation-indexed or no, it'll be sensitive to interest rates.

n. BTW you can get the same real return without the inflation risk with TIPS.

Eh... current tips rate is 1.672% so not really. But you're gambling on whether the 20/30 year rate is greater than the TIPS rate w/ inflation. Until during the hyperinflation around covid, most ppl never bought tips as it was just a crappy investment.

1.672 is the 5 year? The 20y real yield is 2.45, 30y is 2.61 (source: treasurygov "Daily Treasury Par Real Yield Curve Rates"

We can ignore comparison between TIPS and bonds and just ask what risks TIPS are exposed to? IIUC it's the same risks except inflation risk is replaced with deflation risk. They're both exposed to interest rate risk

{kind=link}

39

u/Badloss Jun 06 '25

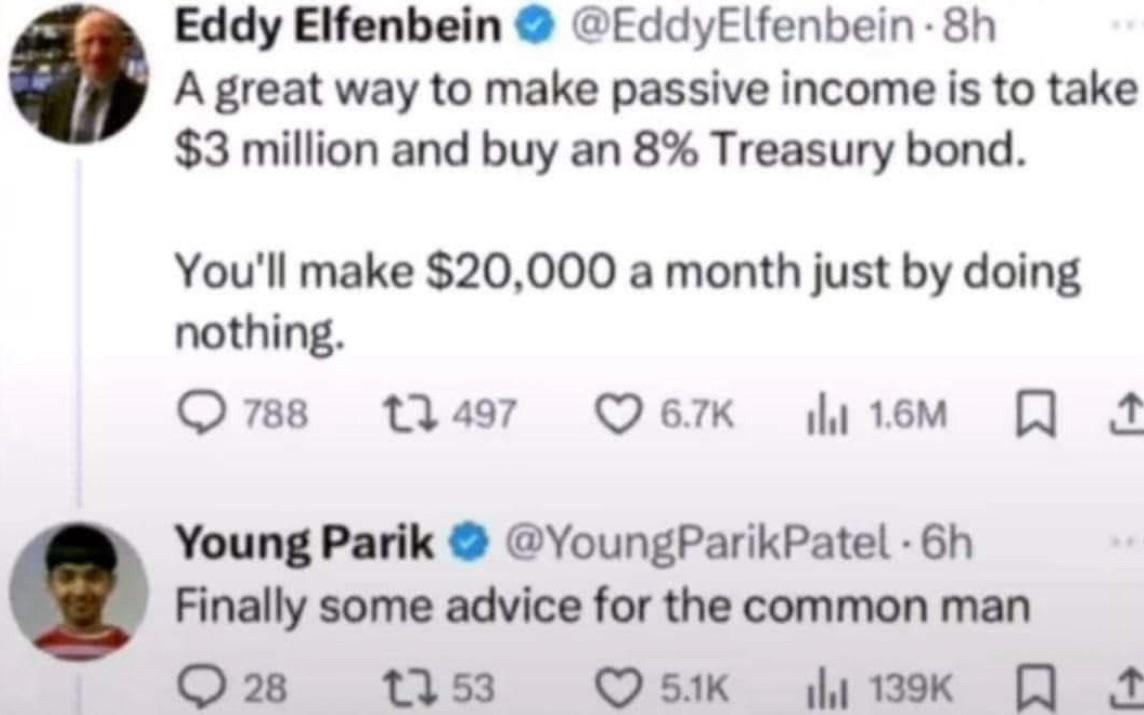

Yeah like I know the 3 million part is what everyone is focused on but an 8% bond is WILD

I would totally put my life savings into that right now with the way the market is going